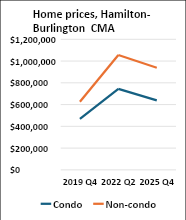

Home prices in the Hamilton-Burlington area continue to decline from the record-high prices of the second quarter of 2022. The median price for a condo is down 14 per cent and the median for other homes is down 11 per cent. But as the chart at right shows, prices are still way up—by a third to a half—from where they were at the end of 2019, just six years ago.

Home prices in the Hamilton-Burlington area continue to decline from the record-high prices of the second quarter of 2022. The median price for a condo is down 14 per cent and the median for other homes is down 11 per cent. But as the chart at right shows, prices are still way up—by a third to a half—from where they were at the end of 2019, just six years ago.

So prices remain sky high. You’d need an income of $146,000 to qualify to buy that median-priced condo and $212,000 to qualify to buy the median non-condo unit. (The median is the price in the middle, with half the homes more and half less expensive.) Median household income for the Hamilton-Burlington area is $98,000.

High home prices are behind the decline in homeownership among every age group except those older than 75 (Census 2021 compared to Census 2011). The impact is largest with the youngest adults, with homeownership among 25- to 29-year-olds down from 44.1 in 2011 to 36.5 per cent in 2021.

Economic uncertainty and high prices are discouraging people from buying—home sales were down nearly a third last year from the peak year of 2021. But lower prices and high costs to build are discouraging new construction, CIBC report asserts. So residential construction workers face layoffs or are shifting to other forms of construction, which may create labour shortages in home construction in future.

As our Affordable Housing Team has recommended, this makes this an ideal time for massive, long-overdue investments in non-market and co-op housing to keep those workers working and to build desperately needed housing for those priced out of the market for for-profit rental or purchased housing. There’s no shortage of need. Dr. Carolyn Whitzman’s detailed calculations showed about 2 million households could not afford rents higher than $1,075 (Census 2021 figures).